The facilities run by utilities and the materials industry are particularly exposed to water shortage. (Photo by ahei via iStock)

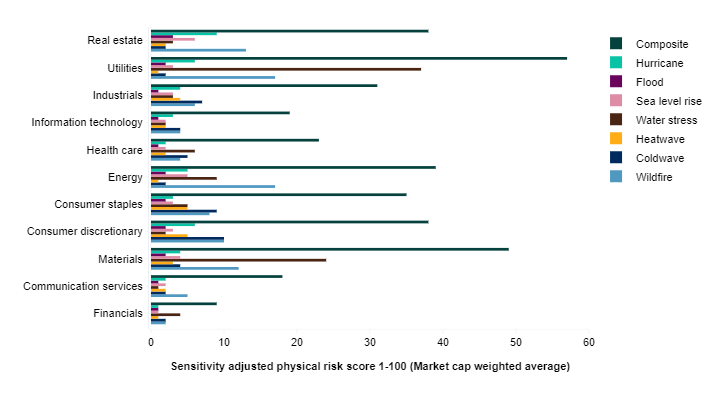

In a comparison of industries, physical assets owned by the utilities, materials, energy, consumer staples and healthcare sectors face the greatest danger from the consequences of a warming world between now and 2050, according to S&P Global Trucost data.

While headline-grabbing events such as hurricanes and wildfires are likely to become more severe and frequent in a warming world, the greatest threat, if left unmitigated, across all industries doesn’t show on many investors’ radar: water scarcity. The facilities run by utilities and the materials industry are particularly exposed to water shortage, exacerbated by shifting rainfall patterns and drought.

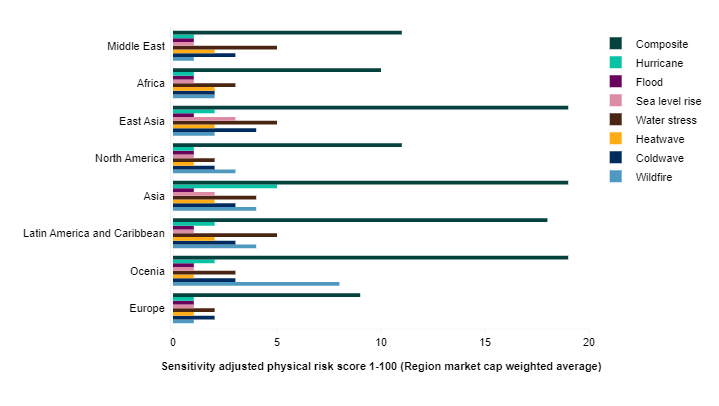

Some regions are in the firing line more than others. The Trucost data, drawn from about 15,000 publicly traded companies representing 95% of global market capitalisation, reveals that business infrastructure located in Asia will bear the biggest brunt of the physical impact of global warming without adaptation, though the projected hit to corporate assets is only marginally lower in East Asia, the Middle East and North America.

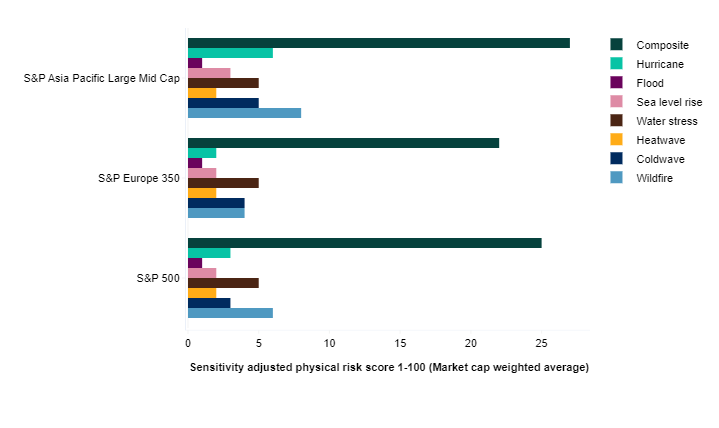

Climate risks facing key S&P indices in US, Europe, Asia in 2050

Trucost’s data comes from publicly available information, licensed datasets and its own models. A score of between one and 33 is low risk, between 34 and 66 is moderate risk, and more than 67 is high risk. The analysis uses sensitivity-adjusted scores to reflect the degree to which each company is exposed to the types of physical risks that are expected to be most material to its business type or model. This is based on company-level data on water intensity, capital intensity and labour intensity.

Water stress reflects the balance between renewable water supply and total water withdrawals (municipal, industrial and agricultural use) within a given area. Water stress can increase due to either a reduction in supply, increasing withdrawals, or a combination of both. For entities located in jurisdictions that draw significant resources, production costs could increase as focus shifts to groundwater supplies when surface water supplies decline.

The latest analysis examines the climate-related threat to corporate assets over the next three decades, from the base year 2020 to 2050, under a moderate scenario for projected temperature increases by 2050.

Corporate assets in Asia face greater physical risk from climate change

Trucost data was used to calculate the risk score for different climate hazards and how they are expected to affect three key S&P indices in Asia, Europe and the US by 2050.

According to the analysis, the S&P Asia-Pacific index faces substantially greater hurricane exposure than the S&P Europe 350 index, while wildfires are a bigger risk factor for the S&P 500 (which tracks US companies). Meanwhile, sea level rise is a bigger risk for the S&P 500 than the European index. Water stress is a substantial risk factor for each of the indices.

Trucost’s hurricane results are a representation of historical exposure as opposed to a projection based on climate change. With extreme weather events expected to become more severe in future, it is important to capture this hurricane risk even though we are not yet able to project for future scenarios.

Scores in this analysis represent a market cap weighted average and are sensitivity adjusted, which means that they are adjusted for expected materiality of each hazard for each of the companies in the index. The composite score is a combination of exposure to the seven climate hazards (heat and cold waves, river and coastal floods, droughts, wildfires, and windstorms), but there will be some companies in each index that will have higher or lower risk exposure.

Assets owned by utilities face biggest physical risk from climate change

The S&P Global Trucost data provides other insights about how corporate assets may stand up to changes wrought by the warming of land, air and the seas. For example, Trucost physical risk data suggests that wildfires, if left unmitigated, will be the biggest physical threat for the real estate industry 30 years from now. Wildfires will also be a major risk factor specifically for the energy, utilities and materials businesses. An August 2020 report from S&P Global Ratings analysts found that physical risks may pose a particular threat to the creditworthiness of issuers within public finance whose locations are fixed, meaning the risk cannot be diversified away.

The impact of wildfires and water scarcity on utilities was highlighted in a new report by S&P Global Ratings. That analysis used Trucost data to explore the climate hazard exposure of 24 large US investor-owned utilities by the year 2050. It found that about 19% of utilities’ transmission lines are highly exposed to wildfires (scoring more than 70 on the one to 100 scale) under both low- and high-stress scenarios.

The report pointed out that all 24 utilities would also face a heightened risk of water shortages. “Utility companies can be highly exposed to water scarcity, and the materiality of this exposure is greater for water-intensive assets, like power plants, in the absence of appropriate adaptation measures,” the report said.

Physical risks may pose a particular threat to the creditworthiness of issuers within public finance whose locations are fixed, meaning the risk cannot be diversified away.

In eastern Asia, the biggest danger is projected to be water stress, resulting from greater heat levels, altered rainfall patterns and high water-extraction rates. Meanwhile, wildfire risks are set to rise significantly in North America and Oceania, which includes Australia.

The peril from climate change has been building for years. In a report published in September 2021, the World Meteorological Organization said that the number of weather-related disasters had risen five-fold from the 711 reported in the 1970-79 period to the 3,165 reported in the 2010-19 period. Global economic losses related to those weather events jumped from $175.4bn in the earlier decade to $1.38trn in the 2010-19 decade.

Such events have triggered significant disruption for corporations and their complex supply chains. Just in the US in 2021, several petrochemical producers were forced to shut down operations in Louisiana ahead of Hurricane Ida’s landfall in August.

And in February, the extreme freeze that hit Texas and other southern US states triggered blackouts, the closure of petrochemical plants, and a sharp spike in the prices of polyethylene, polypropylene and other chemical compounds, according to Platts data.

Attributing a specific weather-related disaster to long-term global warming can be a tricky proposition. But the science is becoming more refined. For example, in an influential report released in August 2021 by the UN’s Intergovernmental Panel on Climate Change, scientists were able to better connect human-caused emissions – primarily due to the burning of fossil fuels – to specific climate and weather extremes, such as heatwaves, heavy precipitation that leads to flooding, droughts and tropical cyclones.

Insurers, banks and other financial institutions are also exposed to the physical risks of climate change. Research from S&P Global Sustainable1, for example, found that as of year-end 2019, the US insurance industry had $582bn invested in some combination of oil, gas, coal, utilities and other fossil fuel-related activities. That marked a slight increase from $519bn in 2018.

The sense of urgency is clear: weather hazards are getting worse, and both businesses and investors need to better understand how corporate assets are exposed to those perils. S&P Global Sustainable1 believes that acquiring a detailed knowledge of those physical risks is vital as stakeholders across the value chain work to mitigate their climate risk and create credible adaptation plans.

Gautam Naik is a senior writer, climate change and sustainability, at S&P Global. Rick Lord is head of innovation methodology at Trucost, which is a part of S&P Global Sustainable1.